In a study whose results reflected the fantastic progress in the consumption of online games via PC and mobile, the company SuperData launched a few hours ago the ‘2020 Year in Review’ document, focusing on the health of digital games and interactive media market, the impact of COVID-19 on games and brands, and gaming trends in 2021.

MORE MOBILE PLAYERS CHOOSING ACTION GAMES

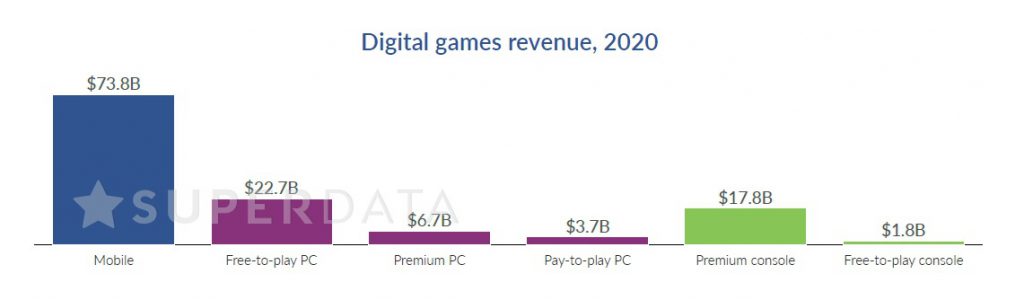

Overall, digital games alone earned US$126.6 billion in 2020, a year where audiences were forced to stay home and interact remotely. In other findings, free-to-play games continued to generate the vast majority of games revenue (78%), with Asian markets accounting for 59% of FTP earnings. Honor of Kings and Peacekeeper Elite, both Tencent titles, each generated over US$2 billion during the year.

The mobile market experienced 10% growth in 2020 and accounted for 58% of the total games market. Despite lockdowns and reduced commuting, mobile earnings remained steady, as a majority of mobile players (62% in the United States) already use mobile devices as their primary gaming platform. Roblox was the third highest-earning digital game of 2020 and surpassed Fortnite thanks to strong mobile growth. Roblox mobile earnings grew as the game creation platform became a social network of choice for young gamers. Although Fortnite still earned more than US$1 billion in 2020, it faced stiff competition from games like Roblox and Call of Duty: Warzone.

Regarding premium games, their earnings grew 28% year-over-year, outpacing the growth of the free-to-play market (9%). North America and Europe together accounted for 84% of all premium games revenue. Since COVID-19 impacted these regions severely, spending on premium content jumped. Life simulation game Animal Crossing: New Horizons became one of the biggest hits in 2020, breaking the console record for premium launch downloads.

VR GROWTH, CONSOLES AND FUTURE TRENDS

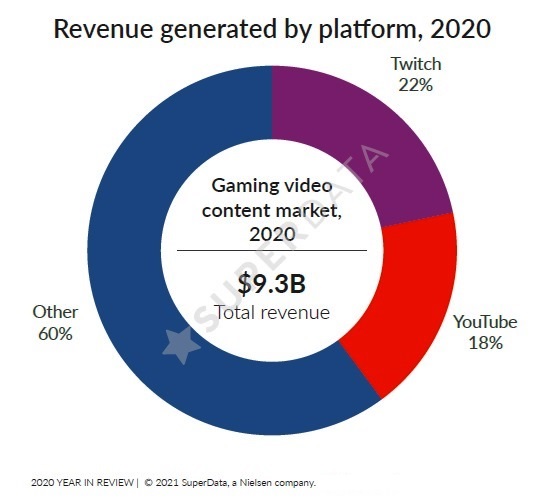

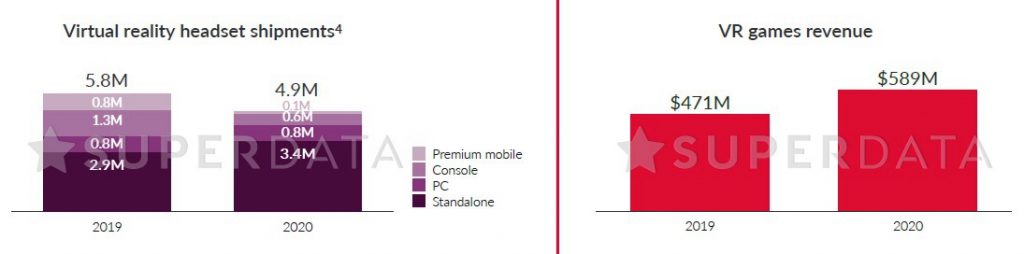

The wider interactive media market also grew on multiple fronts during 2020. Gaming video content (GVC) became a US$9.3 billion industry in 2020, reaching 1.2 billion viewers. Alongside the standard fare of competitive titles and social games, brand crossovers like Fortnite X Marvel and public figures like Congresswoman Alexandria Ocasio-Cortez earned top views. GVC also helped Among Us become one of the most popular games of all time. XR (virtual reality and augmented reality) earned US$6.7 billion in 2020, as VR game earnings jumped 25% year-over-year to US$589 million in 2020. The release of Half-Life: Alyx reinvigorated interest in the technology among hardcore gamers. Additionally, the untethered and budget-friendly Oculus Quest 2 headset attracted everyday consumers to VR.

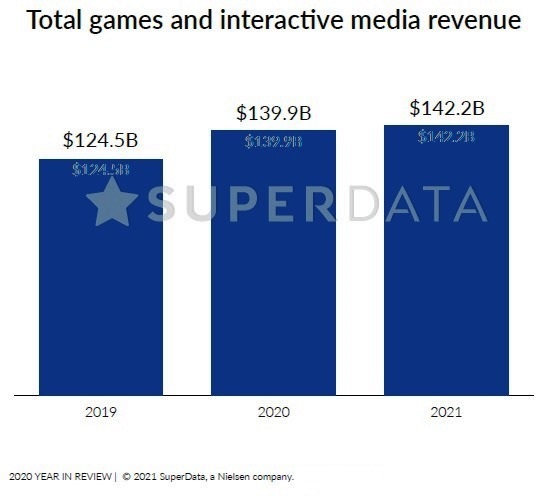

After significant pandemic-fueled growth in 2020, SuperData predicts that interactive entertainment earnings will rise 2% in 2021. Despite an increase in gaming activity due to COVID-19, the rollout of a vaccine is not expected to cause a gaming crash. Although digital game revenue is projected to be roughly flat in 2021, the long-term habits formed during lockdown are here to stay. Notably, both free-to-play and premium markets in Asia were up year-over-year by 11% and 20%, respectively, despite several countries, particularly China, dealing with COVID-19 more quickly and effectively than other markets.

The strategies of the “big three” console makers will continue to diverge. Microsoft is focused on turning Xbox Game Pass into a Netflix of games that runs on everything from phones to Smart TVs. The demand for the service is evident. Revenue and subscriber numbers were up 179% and 175%, respectively, year-over-year in November 2020. Meanwhile, Sony and Nintendo will continue to focus on platform exclusives which drive hardware sales. Industry consolidation will continue in 2021, as developers and publishers fight for a spot in a competitive market. In 2020, announced acquisitions included ZeniMax Media (Bethesda) by Microsoft, Codemasters by Electronic Arts and Daybreak Games by EG7. As game budgets keep on expanding and user acquisition costs rise, smaller companies will continue to be acquired as the top firms seek to broaden their offerings.