Based on a recent survey among 13,246 gamers across nine markets, Facebook presented ‘Games Marketing Insights for 2021’, a document to better inform companies of the sector about new trends and recommend actions to take regarding games development, growth and monetization. This new research into players’ behaviors, including motivations, preferences and habits of new and existing players in markets such as the United States, the United Kingdom, Canada, France, Germany, South Korea, Japan, Vietnam and Brazil, also considered time spent across different gaming devices, monetization behaviors and social engagement.

All participants were divided into two groups: a) New players: people who didn’t play mobile games before the initial peak of the pandemic, and continued to play at least an hour a week (July 2020); and b) Existing players: people who played mobile games both before the initial peak of the pandemic and continued to play at least an hour a week (July 2020).

PANDEMIC SITUATION BOOSTED GAMING NUMBERS

During the last year, there has been an unprecedented surge in consumer demand and disruption to previous consumption habits, as people looked for new forms of entertainment and ways to stay connected with others. More people were playing, watching and streaming than ever before, bringing in new gamers as well as reengaging lapsed players. Developers, publishers and marketers have sought to understand evolving gaming motivations, drive new user acquisition, retain player engagement and, ultimately, understand how this global macro shift will affect gaming business health long term.

Some of the most relevant conclusions of the Facebook text are the following: a) The year 2020 brought new and different gamers; b) The number of people playing mobile games significantly increased across the globe as a result of COVID-19; c) The increase doesn’t seem temporary; d) Many mobile gamers who started playing after the initial COVID-19 outbreak are still playing today, and e) 70% of people report spending more time on mobile devices.

In terms of the mobile gaming modality, new gamers (people who started playing after the outbreak) are significantly younger than existing players (people who were playing before) in the US, UK and Germany. They show more “core” behaviors in terms of genre preferences, engagement, and propensity to play non-mobile games. Familiarity is becoming increasingly important for mobile game discovery, with only a quarter (or less) of people saying they’ve tried mobile games they’ve never heard of. Community activities outside of gameplay increased throughout 2020, with streaming platforms (such as Twitch, YouTube Gaming and Facebook Gaming) seeing record viewing hours. At the same time, while new mobile gamers still prefer to play solo, they’re more likely to engage with multiplayer and social features than existing players.

NEW & EXISTING GAMERS’ BEHAVIORS

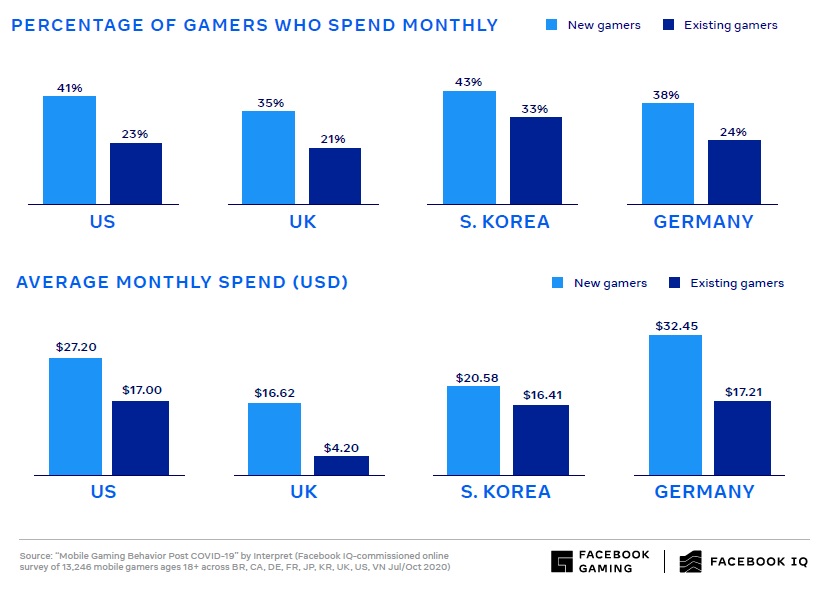

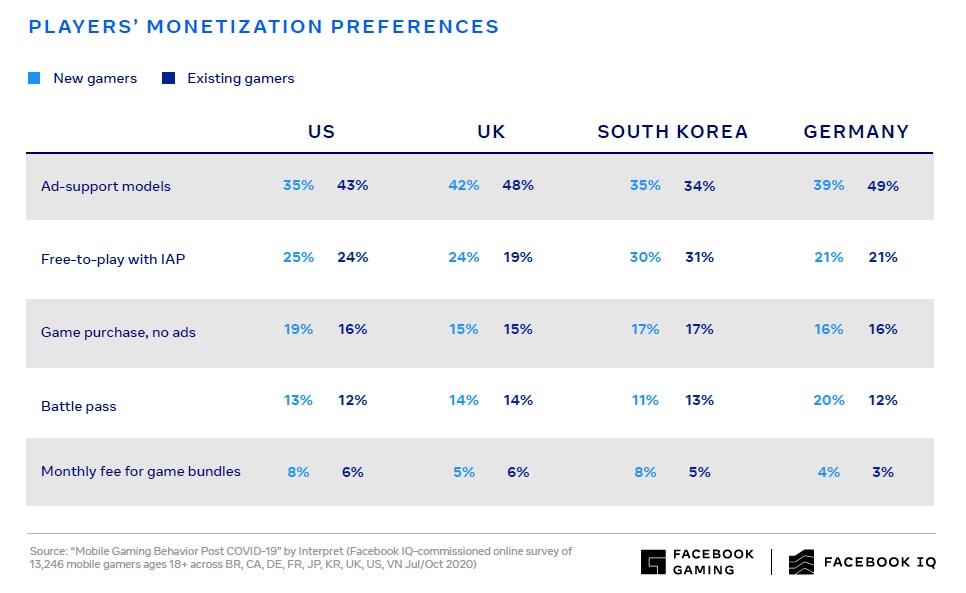

Across all markets, new and existing gamers cited similar reasons for playing mobile games. Relieving stress, passing time, and generating a sense of accomplishment were consistently the top three reasons. The main reason new gamers started playing during the pandemic was because they had more free time (41%). Other reasons included looking for ways to distress (16%), and it was simple and easy to start playing (11%). Compared to existing players, new gamers were significantly more likely to report spending money on mobile games after the initial COVID-19 peak in all markets. They also reported spending more money per month on mobile games. In the US and UK, people were particularly motivated to pay to remove ads. Moreover, in the US, UK, and Germany, new gamers are significantly younger than existing players. The gender distribution of both cohorts is similar in all markets. In the US, new gamers are more likely to own a gaming console (new gamers 64% v. existing gamers: 58%). There were no differences in the UK (66% v. 64%). In the US and UK, new gamers were more likely to spend time playing video games on a PC or gaming console. New gamers play more hours a week than existing players in all markets. Their favorite genres skewed significantly more core than existing players in the US and the UK. Another interesting issue is that new gamers are open to social activity, willing to have cooperative, multiplayer experiences and chatting with others in-game compared to existing players. Mobile gamers across all markets say they prefer free-to-play, ad-supported games. In the US, UK, and Germany, the preference for ad-supported models was stronger in existing players. New players, on the other hand, were more open to alternative monetization models, such as in-app purchases.

Regarding purchasing behavior, in all countries researched, new mobile gamers spend more money in-game than existing players. The latter are more engaged than before COVID-19, yet less likely to report spending money on mobile games compared to before the outbreak. As for online purchases, also grew as consumers expressed concern about going into physical stores.

SHIFTING HABITS, ENGAGEMENT AND MARKETING RECOMMENDATIONS

Facebook also looked at how existing players’ behavior has shifted from before COVID-19 to after. The company asked gamers to describe the impact of the pandemic on their gaming habits in their own words. “Instead of meeting friends in person, I’ve been connecting with them through mobile games. Before COVID-19, it was about 50-50 split between meeting them in person and connecting with them online. Now, it shifted much more towards the online hangout,” some gamers said. In all countries, gamers reported that they currently spend more time gaming than they did pre-pandemic. A large portion of these gamers in each market also responded that their individual gaming sessions are longer (US: 40%, UK: 40%, South Korea: 53%, Germany: 30%).

Community has always been a huge part of gaming. Millions more people are playing games and this, in turn, is contributing to an even greater gaming community. With the influx of new players, general gaming activity outside of in-game saw an uptick in tandem. The number of gaming Facebook Groups grew, streaming sites saw unprecedented surges and anticipation for new releases reached fever pitch. Active members in gaming Groups on Facebook, as well as the number of Groups, propagated during the months following the outbreak, as people connected with their gaming communities. Currently, there are more than 230 million people who are active members in over 630,000 gaming Groups on Facebook per month. From January to August 2020, over 185,000 new gaming Groups were created and over 130 million members joined gaming Groups. In the US, UK, and Germany, this increase was largely composed of 25-34 year olds, while in South Korea, more than half of new members were between 18-24.

After all of this shared data, the Facebook report offers some recommendations to marketing teams of gaming developers, publishers and providers. The increasing engagement with Groups is an opportunity to create two-way dialogue with players, and to foster and encourage community while creating organic conversations. It’s a low-cost way to contact with users to monitor engagement and title resonance. In this sense, companies should design and develop their games with these new audiences in mind, taking into account their core tendencies. These gamers are open to seeing ads, as well as make in-app purchases. Marketers should consider adopting a mixed monetization model to take advantage of this increased engagement. More people are taking part in in-game events and out-of-game activities, especially among the new gamer cohort. This creates new opportunities for to embrace a constant beat in the marketing strategies. A good idea is to join the conversations where gaming communities are gathering to keep audiences engaged via in- and out-of-game activities.

Survey respondents assured that, to buy new games, familiarity and recognition with titles and developers are a key to boost a purchase decision. Console gamers said the most recent game they purchased was the latest edition of a game franchise owned before. Title/brand recognition is leading to discovery and driving sales. Considering these behaviors, companies should build familiarity through awareness, recognition, and distinction. Mobile game marketers can learn from the console industry when it comes to storytelling, understanding that people like to see gameplay in ads. By telling rich stories through immersive experiences and new formats, marketers can create familiarity. The creative elements in ads, added with other attractive means of engaging players such as streamer partnerships, can have the potential to influence prospective gamers and boost business.