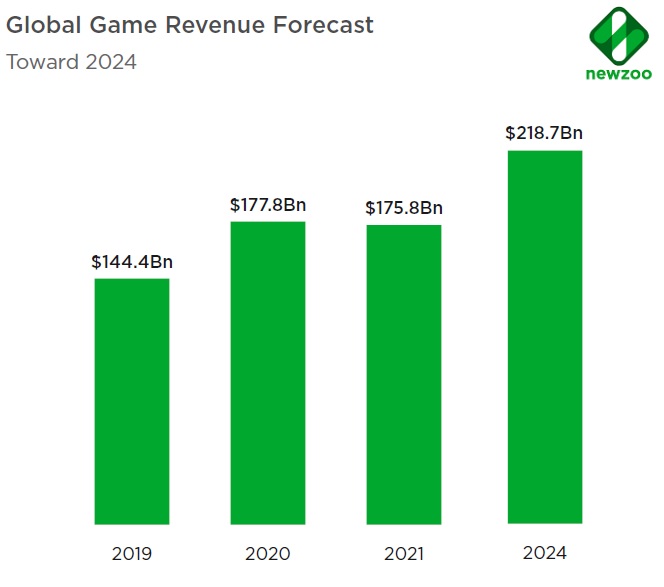

Powered by just under 3.0 billion gamers, the global games market will produce US$175.8 billion via consumer spending in 2021, representing a slight -1.1% year-on-year decline. This decline is temporary and the future of the market is bright, according to ‘Global Games Market Report. The VR & Metaverse Edition’, a recent analysis from well-recognized consultant company Newzoo. Besides, the games market will swiftly recover from its minor 2021 fall. Internationally, the market will grow with a CAGR (2019 to 2024) of +8.7% to reach US$218.7 billion in 2024, passing the coveted US$200-billion threshold in 2023.

The research was conducted from late January to early April 2021, with more than 72,000 invite-only respondents across 33 key countries/markets, gamers aged between 10 and 65. The LatAm countries included on this study were Argentina, Brazil and Mexico.

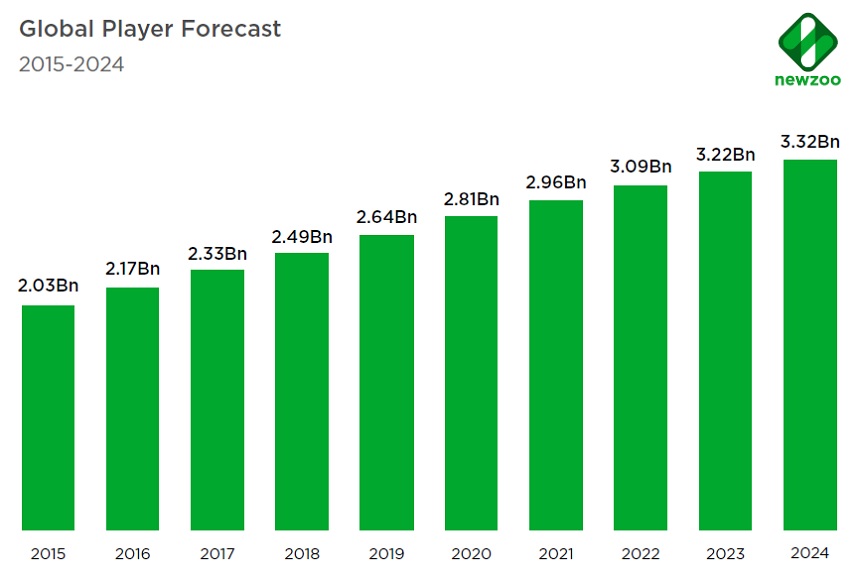

Looking ahead, the global number of players will pass the 3-billion milestone in 2022. This number will continue to grow at a +5.6% CAGR (2015–2024) to 3.3 billion by 2024. Player growth is slowing down as more and more of the world gains access to (mobile) Internet. By 2024, the growth rate for players will be reduced to +3.2%.

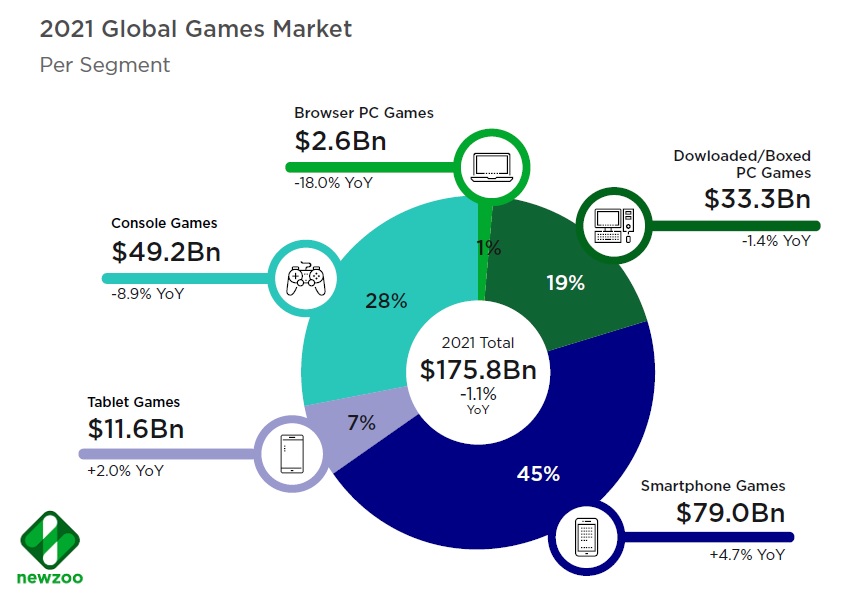

By segment, most players enjoy mobile gaming. In 2021, 2.8 billion out of nearly 3.0 billion gamers will play on mobile. The segment is on track to grow 4.4% year on year to US$90.7 billion in 2021. By 2024, there will be 3.1 billion mobile players, surpassing the 3-billion limits. In comparison, there will be 1.4 billion PC players in 2021, which includes browser players that are slowly migrating to mobile. Console will be played by 871 million people in 2021. In the way of recovering and facing different challenges, 2021’s console market will decline 8.9% year on year to US$49.2 billion, while PC will drop 2.8% to US$35.9 billion. The vast majority of this number (US$33.3 billion) will come from boxed/digital PC games, with browser games accounting for the remaining US$2.6 billion. Growth for both these segments (console and PC) will resume after this year. The number of console players will continue to increase toward 2024, particularly as console gaming gains ground in markets such as China and South Korea, where console gaming traditionally did not thrive.

REGIONS AND COMPANIES

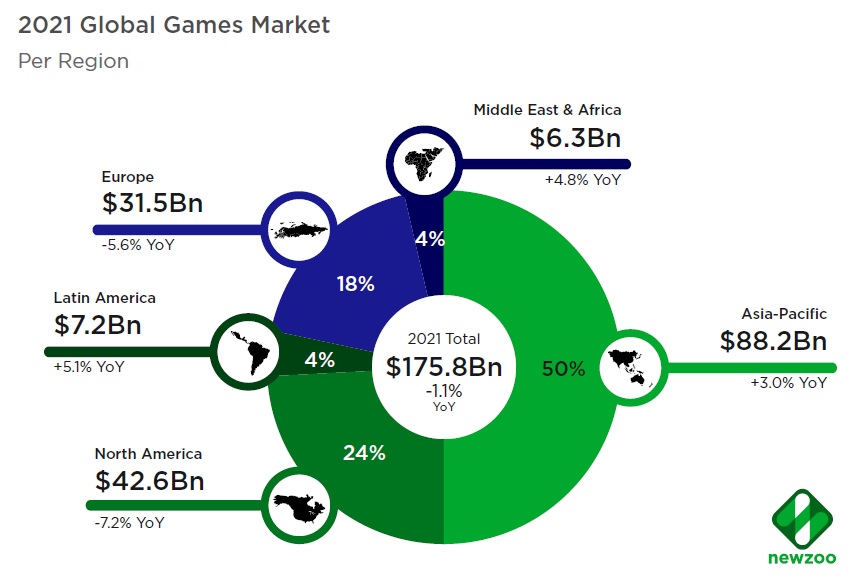

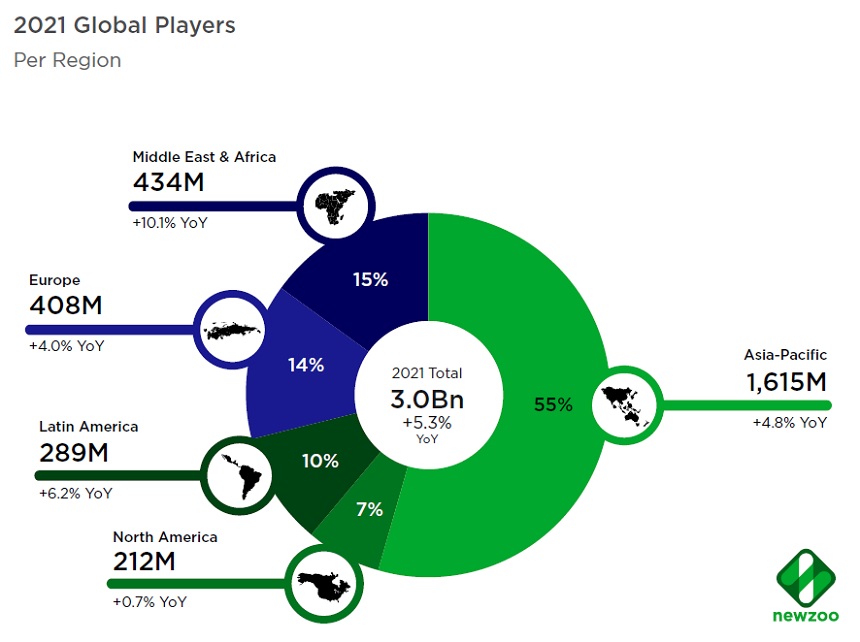

Asia-Pacific and North America will account for 50.2% and 24% of game revenues in 2021, respectively. Both these shares will shrink marginally until 2024, as markets in Latin America and the Middle East and Africa continue along their growth trajectories. Asia-Pacific is easily the world’s biggest region by games revenues, with US$88.2 billion in 2021 alone. With its contribution of US$45.6 billion, China is by far the primary driver here. Owing to the region’s massively mobile-first games market, Asia-Pacific was less impacted by COVID-19. More affected due to its bigger emphasis on console, North America remains 2021’s second-biggest region, boasting game revenues of US$42.6 billion (mainly from the U.S.). Both Asia-Pacific and North America are on track for solid growth, with healthy CAGRs of +8.7% and +7.9%, respectively.

Growth rates are, of course, far above the global average in promising regions such as Latin America, the Middle East and Africa, meaning their overall revenue shares will increase toward 2024. Like North America, Europe was also particularly impacted by the pandemic, with revenues declining 5.6% between 2020 and 2021. However, progress will be strong from 2021 to 2024, when the region’s share of global games revenues will steadily increase.

There will be close to 3.0 billion players across the globe in 2021. This is up +5.3% year on year from 2020, showcasing that 2020’s gaming boom has led to a lasting increase in players, with room for further advance. As is the case every year, primary drivers for player growth are an increase in the online population, better internet infrastructure, and affordable smartphone and mobile Internet data plans. These drivers are particularly impactful in developing regions such as the Middle East, Africa and Latin America, which are the fastest-growing regions by number of players. Asia-Pacific, which also contains growth regions such as Central and Southern Asia, and Southeast Asia, houses the most players by far: 55% of the world’s players live in the region.

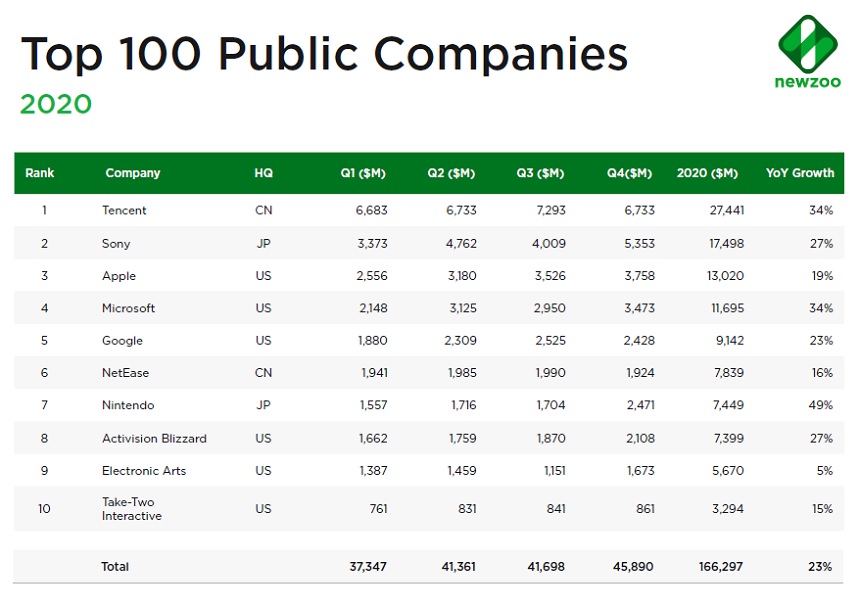

Regarding publishers, Newzoo has ranked top 100 gaming companies. These top 100 public game companies produced revenues of US$166.3 billion in 2020. This marks an impressive +23% year-on-year evolution, and represents 94% of 2020’s games market revenues (excluding advertising). The top 100 accounted for roughly 93% of revenues in 2019, signaling that 2020 was a particularly strong year for larger games companies. Chinese tech giant Tencent, which owns Riot Games and boasts stakes in some of the market’s biggest companies, is by far the strongest games company. Tencent amassed games revenues of US$27.4 billion last year, +34% year on year and almost US$10 billion more than the #2 company by revenues, Sony. Following companies in the top 10 are Apple, Microsoft, Google, NetEase, Nintendo, Activision/Blizzard, Electronic Arts and Take-Two Interactive. Six of the top 10 companies are from the U.S., two from China and the other two from Japan.