Internationally recognized market research firm Newzoo has presented its Global Games Market Report 2023. The study explores the most important trends shaping the gaming industry, including the live-service gaming boom on PC and console, the rise of complementary gaming devices, policies defining mobile gaming, what’s happening with virtual and extended reality, the impact of generative AI in game development, and more.

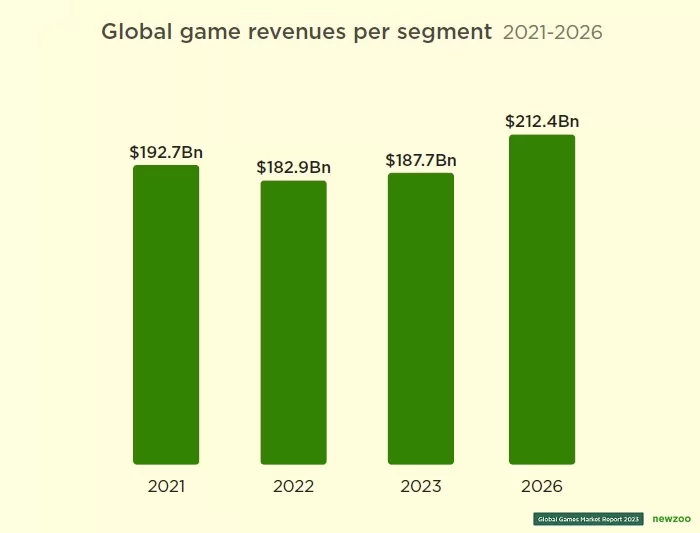

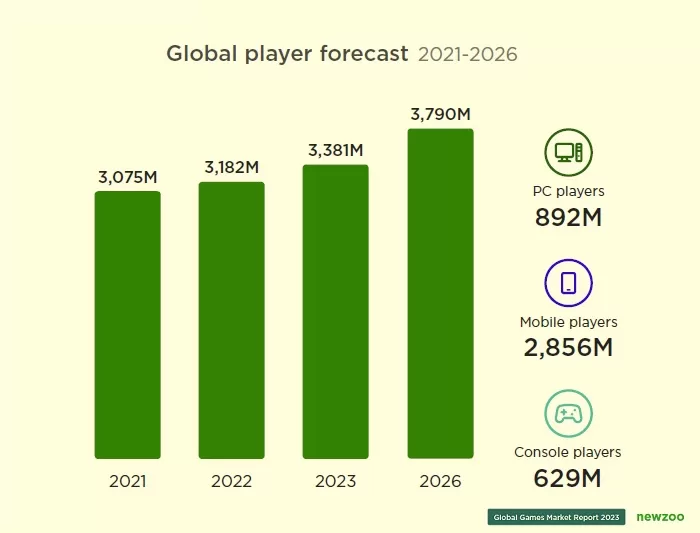

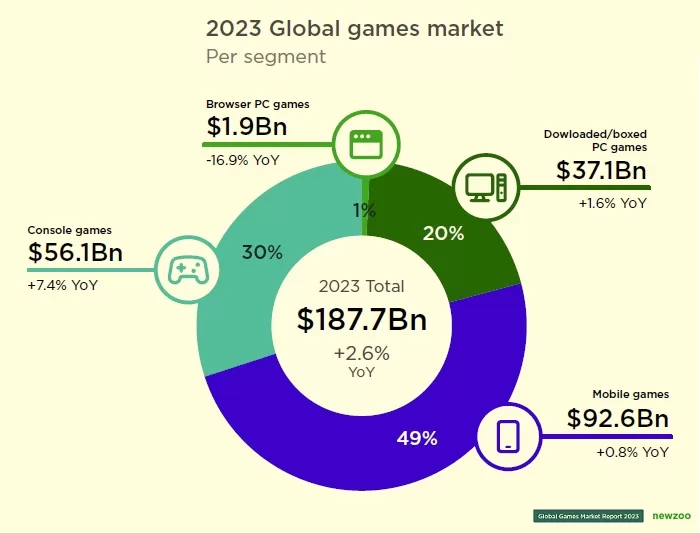

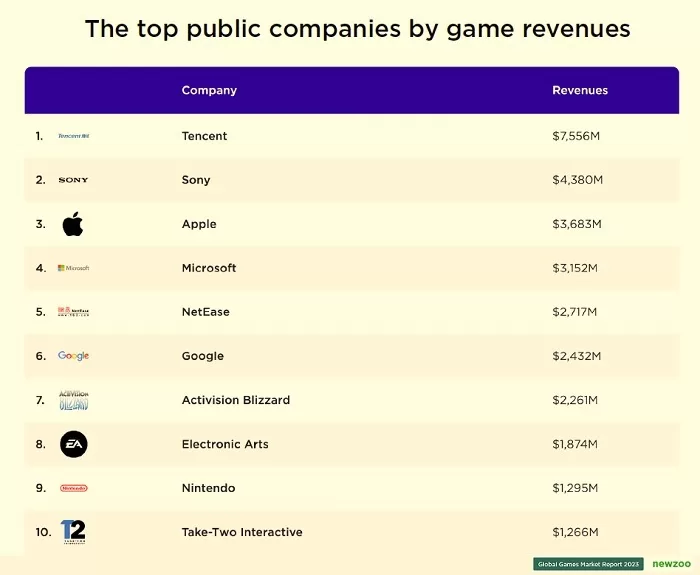

In terms of expanding trends, the document shares that by the end of 2023, the global games market will generate revenues of USD 187.7 billion, with year-on-year progress of 2.6%. The number of players worldwide will reach 3.38 billion in 2023, rising by 6.3% year-on-year. Mobile revenue will increase by 0.8% to USD 92.6 billion compared to 2022, while consoles are expected to produce USD 56.1 billion in revenue (+7.4%) and drive growth this year, due to the release of delayed titles, including Hogwarts Legacy, Zelda: Tears of the Kingdom, and Final Fantasy 16 in H1, followed by Spider-Man 2, Starfield, and Super Mario Bros Wonder in H2. The main public companies by game revenues are Tencent, Sony, Apple and Microsoft, topping the charts in 2023.

MARKETS AND TITLES

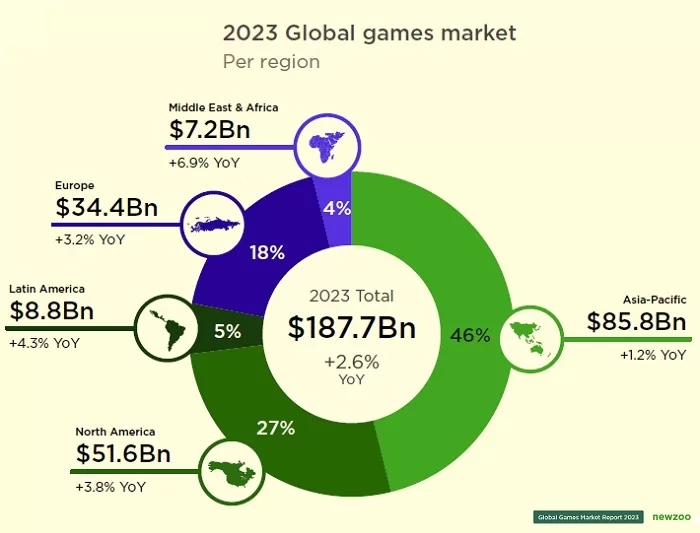

Moreover, Newzoo’s coverage includes 35 countries and markets, showcasing which regions are experiencing rapid growth and which may still have a ways to go in shaping the global markets. The Asia-Pacific (APAC) region will lead the global market with USD 85.5 billion in revenue, up 1.2% year-on-year. For their part, the Middle East & Africa and Latin American regions will grow gaming revenue by +6.9% and +4.3%, respectively (the greatest progress among all continents). Console gaming will increase consumer spending in the Western market, forecasting revenues of USD 51.6 billion in North America, up 3.8% year-on-year, while Europe is expected to elevate 3.2% to reach USD 34.4 billion.

About players, from the total of 3.38 billion for 2023, APAC represents the 53% with 1.79 billion (+5.7% YoY), followed by Middle East & Africa (574 million), Europe (447 million), Latin America (335 million) and North America (237 million). Again, Middle East & Africa (+12.3% YoY) and Latin America (+6.1% YoY) will enjoy the largest player expansion in 2023.

Looking ahead, Newzoo said the global games market is likely to reach USD 212.4 billion in revenue by 2026, stressing the continued sale of the current-gen consoles and the successor to the Nintendo Switch as major factors.

DEI AND GAMERS BEHAVIOR

In parallel, recently, Newzoo added some broader Diversity, Equity & Inclusion (DEI) related questions to 2023’s Global Gamer Study. Understanding how DEI themes and initiatives shape the industry is an important factor in making games more inclusive and accessible for all types of players. The Global Gamer Study helps companies identify their most valuable target audiences across 36 markets.

Globally, 64% of gamers indicate (agree/strongly agree/completely agree) that diversity in games is important to them. The share rises when it comes to younger gamers. This suggests that younger generations of gamers perceive diversity in games as more relevant to them than the preceding generations.

When checking this data by generation, we see that 71% of Gen Alpha (people born between 2010 and 2023, 1 to 13 years old) indicate (agree/strongly agree/completely agree) that diversity in games is important to them. This share drops to 50% for Gen X (1965 to 1980, age range 43-58 years old) respondents and 35% for Baby Boomers (1946 to 1954, age range 69-77 years old).

While nuances exist across different markets and generations of players, representation in video games matters across the global gaming audience. Globally, 62% of players agree (agree/strongly agree/completely agree) with the statement that they feel well-represented in the games they play. Considered by generation, a smaller share of older players agree that they feel well-represented in video games, suggesting that older generations feel less represented in games than younger players. In fact, 72% of Gen Alpha players indicate that they feel well-represented in the video games they played, a far higher share than Gen X (48%) and Baby Boomers (35%).

If we look at the game features players find most appealing, we see that 18% of all gamers select “Diversity of characters within a game” (i.e., representation of ethnicities, genders). This share varies by generation: 22% of Gen Alpha gamers find character diversity appealing, while 6% of Baby Boomers share this feature preference.

Finally, over half (57%) of the players covered in the Global Gamer Study agreed that they did not play certain games because they didn’t feel they were made for them. Interestingly, the share of players who approved this statement remained relatively consistent across all generations, ranging from 54% to 58% of players.