According to projections of recent 2023 Gaming Spotlight report from market analyst firm Data.ai and its partner IDC, mobile gaming will eclipse 56% market share of global consumer spend in gaming for 2023, compared to 22% for console game revenue, 21% for PC/Mac, and around 1% for handheld console.

Estimations say that, by the end of this year, revenue from mobile gaming will reach USD 108 billion. For its part, the console market is poised to hit USD 43 billion, up 3% year-over-year. The growth is attributed to the rise in spending for Sony’s PlayStation 5 and Microsoft’s Xbox Series X|S consoles. PC/Mac games market revenue will increase 4% year-on-year to USD 40 billion this year. Finally, global cloud-streamed gaming is expected to bring in USD 3.8 billion across all platforms. The study says subscription-based game earnings will lead consumer spending in the sector.

2022 was, overall, a down period for gaming spent on mobile. It represented the first year-over-year decline in revenue for the category since the advent of the app stores. This year has seen a potential bottoming out of that decline, with signs that a new period of growth may be on the horizon even if 2023 comes in slightly lower than last year in total.

About markets, South Korea recently accounted for the gains in market share for mobile spending in APAC. Brazil, Turkey and Mexico led growth in the Rest of World.

PERFORMANCE OF GENRES AND TITLES

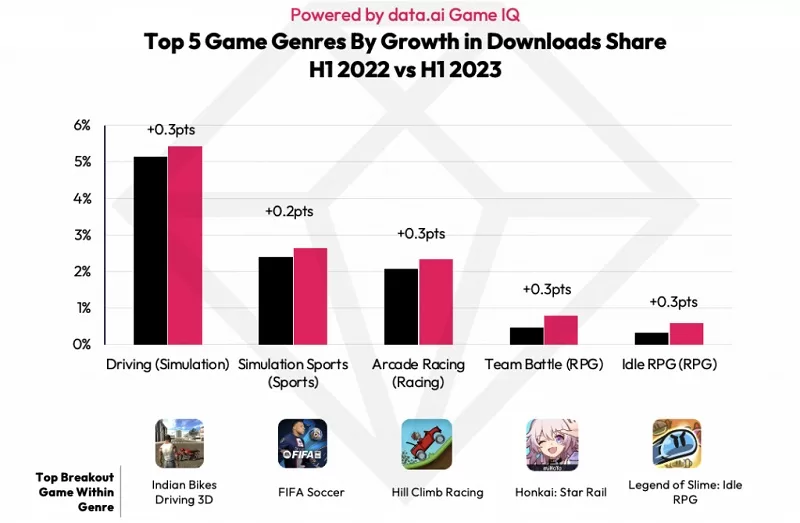

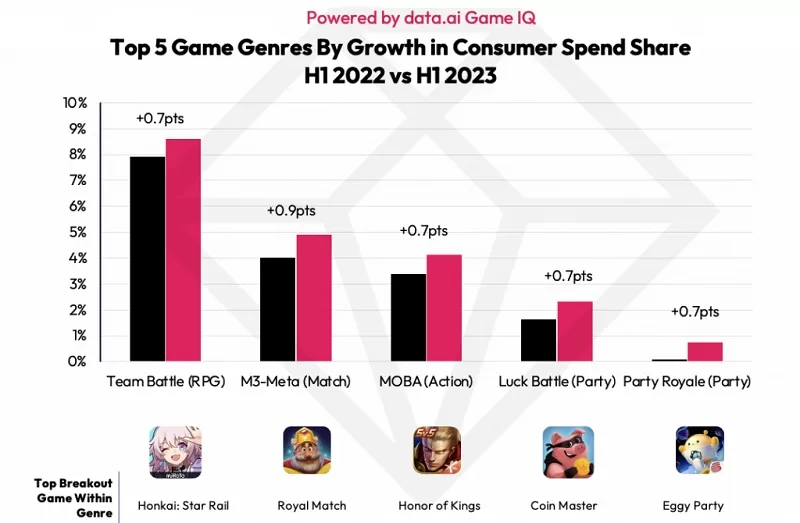

One aspect of this analysis looks at shifts in market share among the various game genres, which is a key to understanding which ones are expressing outsize growth even as the overall market has contracted from the high points witnessed in 2021. These shifts were minor in the grand scheme, reflecting fractions of percentage points, yet are still helpful in deciphering consumer affinity as other signals diminish, particularly in mobile games.

Looking at downloads, Driving and Sports Simulations posted the strongest showings in terms of year-over-year growth, while revenue share was redistributed towards Team Battle and M3-Meta, led by games like Honkai: Star Rail and Royal Match, respectively.

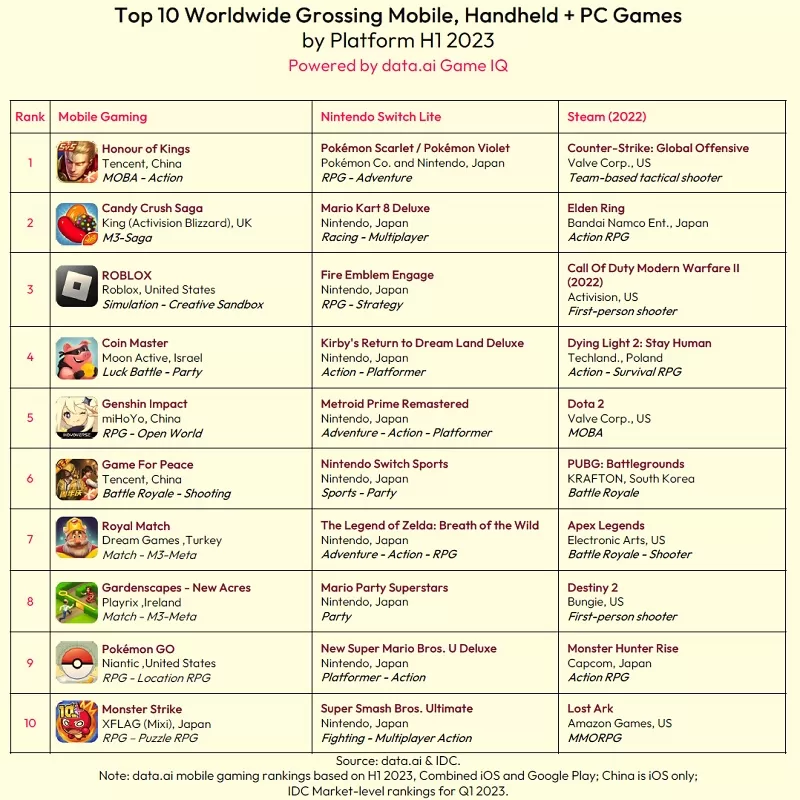

Exploring beyond genres, the Gaming Spotlight goes inside the data to identify the most successful breakout mobile titles so far in 2023. Games that performed well in H1 2023 were varied, including the launch of a board game (Monopoly GO) turned on-the-go mobile experience, a highly anticipated RPG release (Honkai: Star Rail) building on the popularity of genre-defining Genshin Impact, a savvy title (Royal Match) disrupting a stable Match-3 market in under three years, and a cross-platform IP franchise based on the world’s most popular sport (FIFA Soccer) seeing renewed fervor from tentpole live sporting events. Strong IP, capitalizing on market momentum and leveraging events are common themes for success.

GAMING ADVERTISING AND MONETIZATION

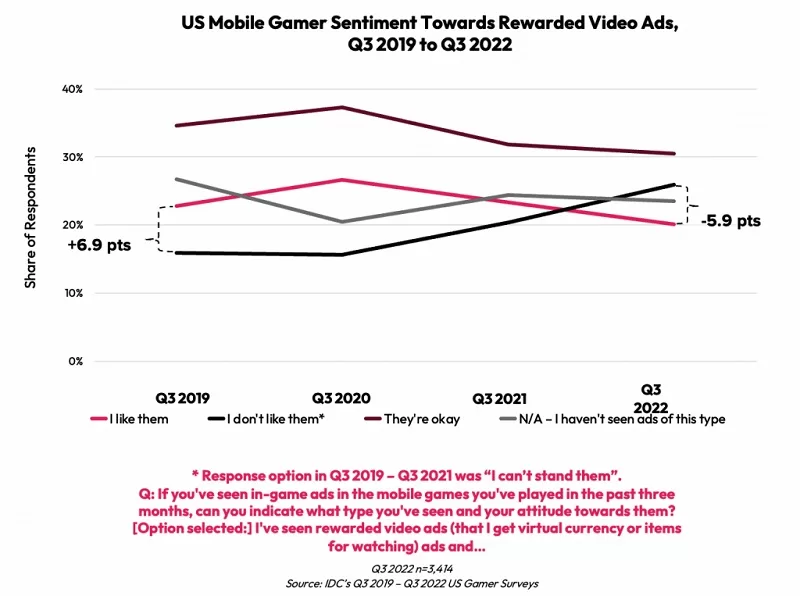

According to IDC, most mobile app and game users (by a 3:1 margin) would rather see ads in exchange for free content and services than to pay for apps and avoid all ads. As a monetization mechanic, info from Data.ai reveals that games which monetize through the app stores are experimenting with hybrid models that include ads as a way to make gaming more inclusive and accessible for the widening gaming audiences, as well as more lucrative for the publishers.

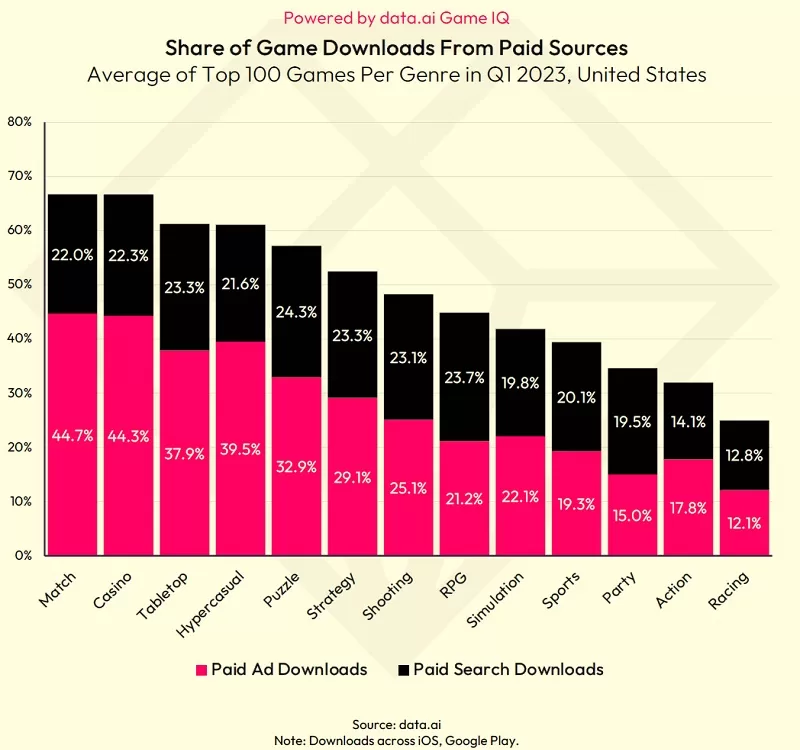

Considering Paid User Acquisition, match, casino and tabletop games lead in paid app installs. In general, the market benchmarks for paid downloads vary both by game genre and country. In addition, some genres are more likely to require paid promotion than others. Overall, Paid App Install Ads (vs Paid App Store Search) tends to contribute a larger portion of paid game downloads.

That being said, the impact of IDFA’s deprecation is apparent, and consumers still favor privacy when it comes to ad tracking, underscoring the importance of contextual market data to inform successful strategies. For gamers specifically, that sentiment towards ads varies dramatically by type. In the U.S., sentiment towards video and banner ads has grown more positive, but still skew more negative overall. Rewarded Video ads remain the most positive for gamers, but sentiment has dipped slightly in 2022.