The past 18 months have been a period of immense global growth for gaming, but what does the future hold for the industry? To answer this question, Google commissioned Newzoo to conduct an extensive market and consumer research in 16 countries across four global regions: 1) North America, 2) Latin America, 3) Europe, Middle East & Africa, and 4) Asia. The result is a set of five groundbreaking documents, under the title: Beyond 2021: Where does gaming go next?

This global gaming market and consumer research text underlines how 2020 saw the global games market increasing 23.1% year-over-year, the highest growth rate in more than a decade. This week, Newzoo revealed that gaming will generate USD 180.3 billion in 2021, an increase in consumer spending of 1.4% year-over-year compared to 2020. For astute industry observers, this is a moment to be optimistic and anticipate where gaming will go next. Globally, the industry is expected to reach USD 218.7 billion in 2024, passing the coveted USD 200-billion threshold in 2023. Also in 2024, mobile gaming will make USD 116.4 billion; the cloud gaming market will amass USD 6.5 billion, while Esports will generate USD 1.6 billion.

DRIVING THE GAMING GROWTH

By the end of 2021, almost three billion players will have spent a combined USD 180 billion on games. Some key themes will continue to play crucial roles in shaping the gaming landscape. To help define their impact, three categories can be distinguished: 1) Novel trends. Examples of consumer behavior towards tech and services evolving in new ways: a. The emergence of games as a social platform and metaverse; b. Audiences’ large-scale adoption of games subscriptions; 2) Accelerated trends. Behaviors that existed pre-pandemic and were significantly boosted by it: a. The rise of streaming as a form of social engagement; b. The move to platform agnosticism, and c. The acceleration of cloud adoption; and 3) Future-proofing the industry.

When asking about players in the future, the study considers that while some (26%+ of new and returning players, and 18% of veterans) are planning to reduce their gaming, there will be a net increase in engagement. For instance, 65-70% of new and returning players esteem to continue playing at the same or a greater level after the pandemic, resulting in a sustainable increase in audience engagement, and 30%+ of players expect to further increase their consumption of streaming and Esports content.

LATAM IS LEADING THE WAY

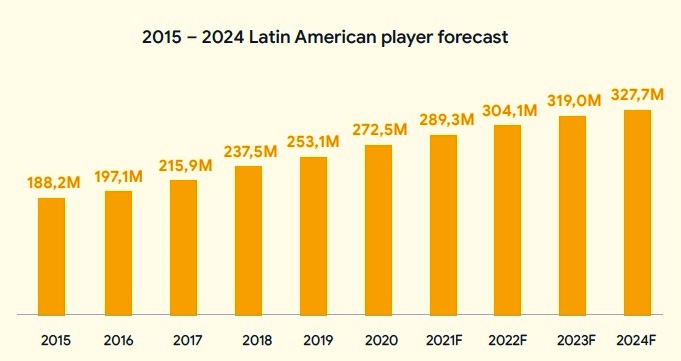

One of the world’s fastest-growing regions, Latin America is a region in transition. Having moved from PC and console to mobile, players want and expect further democratization of access to games. With the largest gaming audience increase of any region from 2015 through to 2024, Latin America also ranks second globally for growth in consumer spending on games (2015-2024), albeit from a small base of 4% of the global games market in 2021. In 2021, 289.3 million LatAm players will spend a combined USD 7.2 billion on games, of which 48% will be spent on mobile, 27% on console, and 25% on PC. With an average age of 34, Latin America has the youngest audience of the four major global regions. It also features a higher percentage of new or returning players compared to more mature regions such as North America.

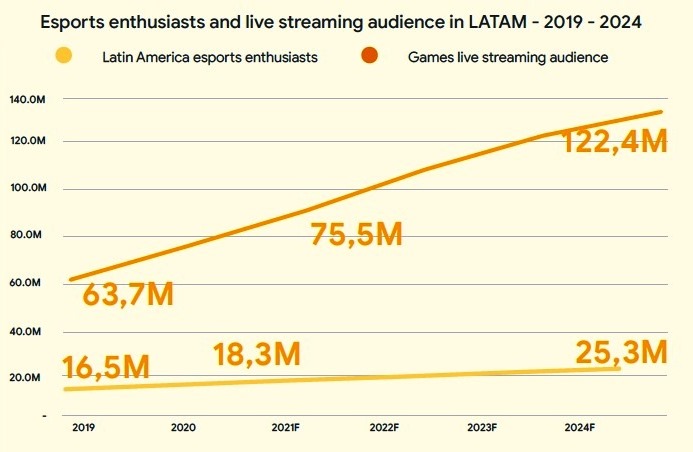

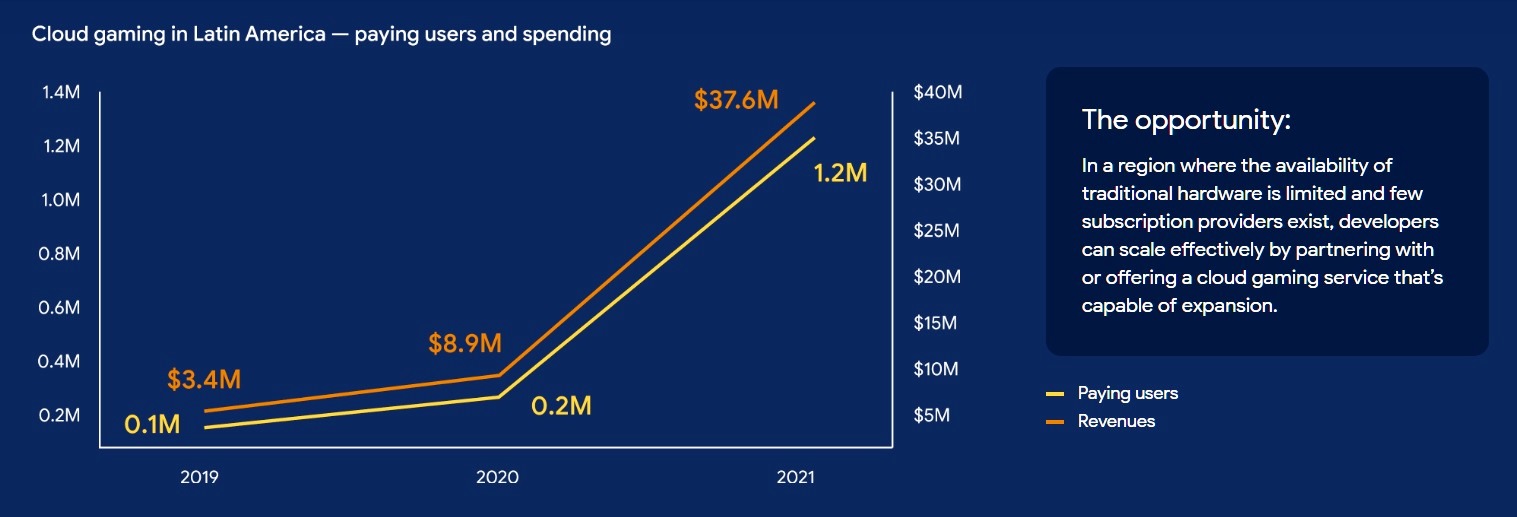

Three themes that will shape the Latin American region beyond 2021 are the following: 1) Mobile gaming is fueling growth in live streaming and Esports; 2) New players and effective monetization strategies will be crucial; and 3) Cloud gaming can solve hardware issues and support subscriptions. Latin American players are watching top-tier streamers and Esports teams in record numbers. As a result, the audience for live-streamed content is expected to rise to 122.4 million people by 2024, by which point the number of Esports enthusiasts will have grown to 25.3 million people. Moreover, LatAm witnessed a huge spike in engagement over the past 18 months. However, this growth has moderated across all platforms in the second half of 2021, with a predicted increase of just 8% between 2020 and 2021. Cloud gaming is an opportunity to democratize hardware usage in the Latin American region where regulation has made ownership difficult. From 2020 to 2021, the number of players paying to use cloud gaming services has grown six fold, to 1.2 million players who will spend USD 37.6 million on access to cloud gaming services and content purchased via those services.

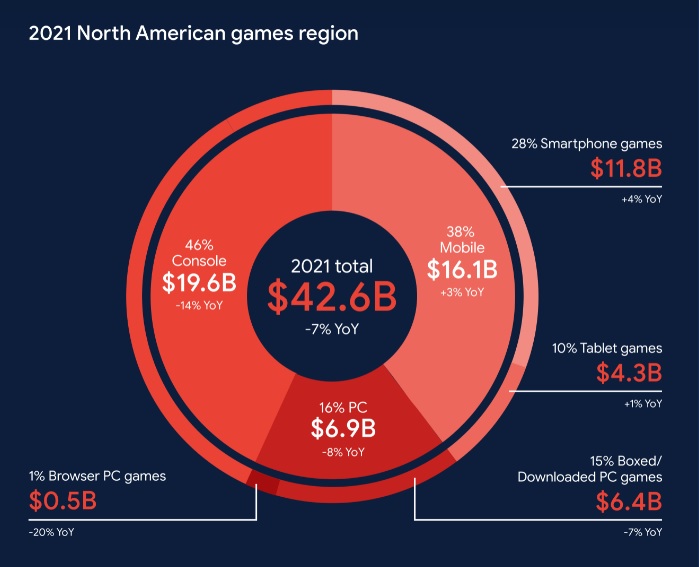

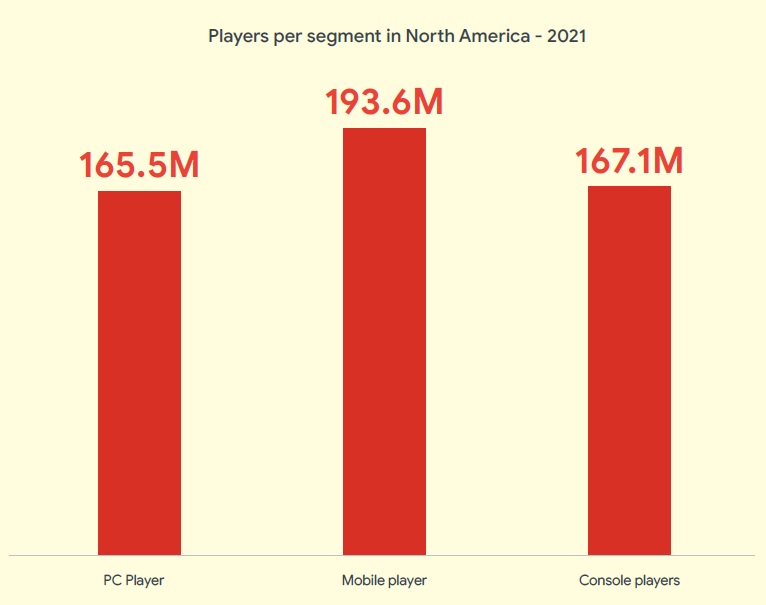

Regarding North America, this mature, console-first region is having a huge increase in mobile gaming and innovation around engagement and monetization. Although is less likely to witness here dramatic advance in numbers of traditional players, interesting experimentation is taking place around engagement and monetization. North America is a region where gaming has already reached near-universal adoption levels, and this has several implications for how it absorbs external shocks such as the events of the past 18 months. In 2021, 212.1 million players in North America will spend a combined USD 42.6 billion on games, with console being the dominant platform. However, like most regions, North America has also seen tremendous upsurge in mobile gaming. The U.S. consumer research from Newzoo found that 83% of respondents were already playing before 2020, the largest such share of all surveyed regions. Another 13% were returning players (those who stopped playing at least once but started again during the pandemic), and the remaining 4% were new players (those who started playing for the first time after February 2020). Three themes that will shape the North American region beyond 2021 are the following: 1) Games have been normalized as a form of social media; 2) Mobile offers opportunities to expand and innovate; and 3) The popularity of streaming and Esports will continue to soar.

igaming, mobile gaming, games, gamers, players, consumer spending, Google Games, Newzoo, video gaming, Esports, Latam, North America, report, time spent, engagement, cloud gaming, trends, streaming, metaverse, console gaming, enthusiasts, monetization igaming, mobile gaming, games, gamers, players, consumer spending, Google Games, Newzoo, video gaming, Esports, Latam, North America, report, time spent, engagement, cloud gaming, trends, streaming, metaverse, console gaming, enthusiasts, monetization

igaming, mobile gaming, games, gamers, players, consumer spending, Google Games, Newzoo, video gaming, Esports, Latam, North America, report, time spent, engagement, cloud gaming, trends, streaming, metaverse, console gaming, enthusiasts, monetization igaming, mobile gaming, games, gamers, players, consumer spending, Google Games, Newzoo, video gaming, Esports, Latam, North America, report, time spent, engagement, cloud gaming, trends, streaming, metaverse, console gaming, enthusiasts, monetization

With the majority of North American gamers already playing on mobile, opportunities for audience growth are limited, but revenue will continue to rise. As we approach 2024, the total number of mobile players in North America is expected to climb at a CAGR of 0.8% to 199 million, and revenue to increase at a CAGR of 6.4%. This degree of development will allow developers to experiment with novel monetization strategies, explore cross-play, and expand beyond mobile audiences. Finally, the North American live-streaming audience will grow to 91.5 million people in 2021, accounting for almost 13% of the global audience. Consumption of game-related content rose by just over 40% in 2020 and is expected to increase by an additional 39% in the future.