Two separate but overlapping regulatory events of recent weeks mean that Canada is set to be in sharp focus for the global online gambling and sports betting industry during the second half of 2021 and 2022. A new analysis from VIXIO GamblingCompliance, a provider of independent legal, regulatory and business intelligence to the global gambling industry, clarifies the implications of recent moves to expand sports betting and Internet gaming made by both the Parliament of Canada and the country’s most populous province, Ontario. Moreover, the text ‘Canada: Opportunities in Online Gambling & Sports Betting’ provides a forecast on the projected size of a competitive online gambling market in Ontario, understanding there are some critical policy factors to monitor, as the landscape for both sports wagering and online casino gaming is redrawn over the coming months.

CHANGE IN LAW AND SPORTS BETTING POSSIBILITIES

On June 29th, Bill C-218, the Safe and Regulated Sports Betting Act, became law, following its approval by Canada’s House of Commons and Senate. Until now, the Federal law has essentially limited Canada’s lawful sports betting market to parlay or multiple bets, predominantly in the form of sports lottery-style games, with legal offerings hamstrung in their ability to offer in-play wagering or the typical variety of bets on single sports games that are available via offshore operators.

Bill C-218 did not actually make any new form of sports wagering legal. It will now be left to each province to decide how, where and when they wish to permit single-event sports betting. In this respect, the situation in Canada is similar to that of the United States, where states have already taken markedly different regulatory approaches since the May 2018 ruling of the U.S. Supreme Court to invalidate the federal prohibition contained in the Professional and Amateur Sports Protection Act (PASPA).

Potential policy options for Canadian provinces when it comes to single-game sports betting include: a) Online sports betting: to be offered either directly through their own state-owned lottery corporations or through a regulatory system involving private sportsbook operators, as is being implemented in Ontario; b) Casino sportsbooks: cross-border casinos in Michigan, New York and soon in Washington State all offer sports betting. Canadian casino operators will likely urge provincial authorities to enable them to host Las Vegas-style sportsbooks at their own facilities; c) Retail locations: in addition to casinos, several Canadian provinces offer video lottery terminals (VLTs) at other retail locations, as well as smaller charitable gambling venues, which could conceivably host sports wagering kiosks operated by lottery corporations.

ONTARIO WILL LEAD THE WAY

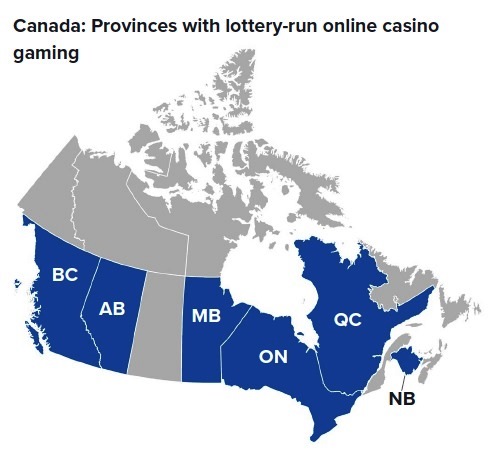

The end to Canada’s prohibition on single-game sports betting will permit the establishment of a first-of-its-kind regime for privately operated online gambling in the province of Ontario. However, regarding online gambling, it has been limited to the current platforms of provincial lottery corporations, such as Ontario’s PlayOLG, the British Columbia Lottery Corporation’s PlayNow, Loto-Quebec’s EspaceJeux or PlayAlberta.

In December 2020, Ontario approved a budget law to establish a new agency to operate Internet gambling through partnerships with a variety of registered private operators. In essence, the new market will be the first European-style licensing regime for online gambling in Canada, albeit under a unique regulatory framework that takes account of further provisions within the federal Criminal Code that require provincial governments to themselves “conduct and manage” most forms of gambling in their jurisdictional borders.

Online gambling will be regulated by the Alcohol and Gaming Commission of Ontario (AGCO), which will register operators and technology suppliers, and establish binding standards to govern their operations. A new independent subsidiary of AGCO, iGaming Ontario, has been formed to serve as the agency that will contract with private operators, receive a share of their revenue and disburse it to the province, and implement uniform operating procedures related to information sharing and player protection.

Unlike in most of the U.S., the Ontario government has signaled that there will be no cap on the number of operators that may compete in a jurisdiction home to nearly 15 million people, with no barriers to market access by way of a requirement to partner with an incumbent land-based gaming entity.

According to VIXIO GamblingCompliance forecasts, the Ontario market will be a lucrative one. It will be able to include full sports betting in addition to casino games and poker. Assuming a late 2021 or early 2022 market launch, a full product range and a competitive effective tax rate in the region of 20%, Ontario’s online gambling market could generate a total gross revenue of C$989 million (US$795 million) in its first year, before growing to C$1.86 billion (US$1.5 billion) by 2026. Depending on future legislative developments to regulate online casino games in further U.S. states, Ontario is set to be one of the largest online gambling markets in North America by 2025, alongside Pennsylvania, New Jersey, Michigan and potentially Illinois.

FUTURE OBSTACLES AND OPPORTUNITIES

In Canada, many doubts remain, and it is important to understand a number of regulatory variables that will define the scope and scale of future opportunities in this market. Some of them can be mentioned here: a) Characteristics of the sports betting model: although Ontario has confirmed its intention to include full sports betting in its plans for a competitive online gambling market, how quickly other provinces follow Ontario in implementing a similar model is very much uncertain. At the very least, some provinces may be more likely to watch and wait in order to learn initial lessons from Ontario before determining whether to open their own online markets to private operators. New lottery-run online sportsbooks are likely to be launched in the near future in British Columbia, Manitoba and Alberta, as well as Ontario, underscoring Canadian sports betting as a more immediate B2B or business-to-government opportunity, at least outside of the country’s largest province; b) ‘Conduct and Manage’ restrictions: although private operators in Ontario will be able to register players through their own branded platforms much like in European or other North American markets, the province must still ultimately “conduct and manage” all online gambling operations in order to comply with Federal Criminal Code of Canada. One question to be answered is whether iGaming Ontario or its contracted private operators will have ultimate ownership or control of player data and how freely operators will be able to use that data to market to their customers; c) A more European than American system: in Ontario, there will be marketing and advertising restrictions for online casino gaming. However, about offshore operators, this province will intend to attract them into the regulated market, with operators not required to cease offshore activities in other Canadian provinces even after being registered in Ontario. That would give current Canadian-facing operators such as bet365, Betway or Pinnacle a significant advantage. Of course, this will generate a stronger competition, with a more diverse betting offering for Canadian players.