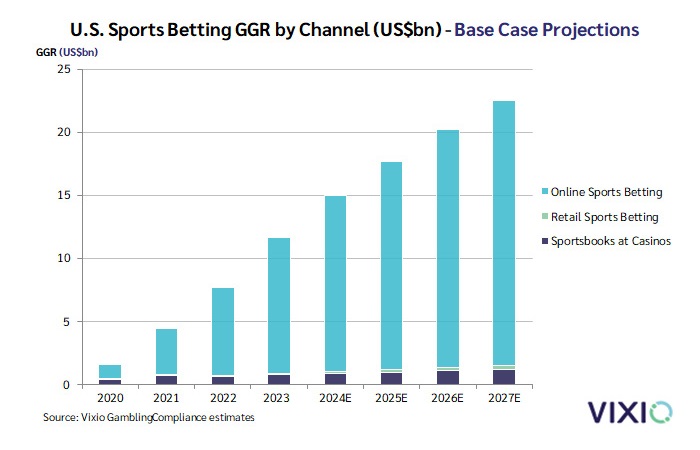

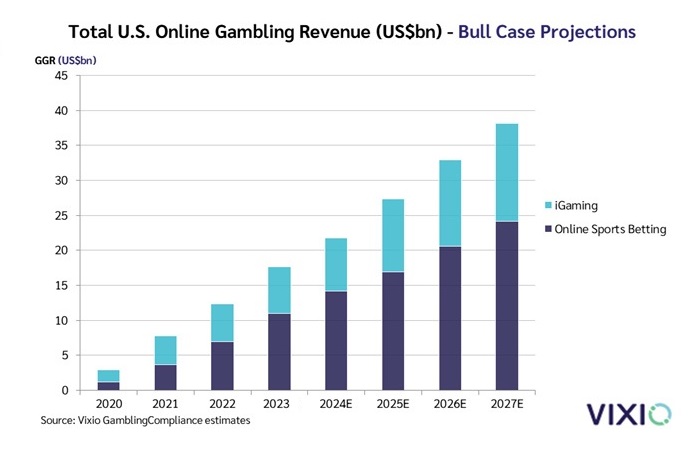

According to Vixio GamblingCompliance forecasts, a relevant provider of independent legal, regulatory and business intelligence to the global gambling industry, the U.S. sports betting market will be worth USD 22.3 billion to USD 24.5 billion in total annual gross revenue by 2027, depending on different business scenarios. Moreover, net gaming revenue, after bonuses and other deductions, will reach USD 16.6 billion USD 18.2 billion by 2027. Meanwhile, total gross revenue from all U.S. online gambling (online sports betting, plus iGaming in certain states) is estimated to reach USD 30.7 billion to USD 35.4 billion by 2027.

Current outlook on commercial gaming

The commercial gaming revenue in the United States accomplished a quarterly record of USD 17.67 billion in Q1 2024, the industry’s 13th consecutive quarter of growth, according to the American Gaming Association (AGA). The quarter was punctuated by March 2024 revenue of USD 6.09 billion, the industry’s second-highest grossing month ever.

Across the country, 11 state gaming markets set new quarterly revenue records, including Pennsylvania and New York, two of the nation’s largest commercial gaming markets. Both retail and online gaming saw annual growth in Q1 2024, though at slower rates than in previous quarters. Retail gaming accounted for 70.7% of total revenue, while online gaming represented its largest share ever, 29.3%.

Meanwhile, iGaming grossed an all-time high of USD 1.98 billion in Q1, a 26.1% year-over-year increase bolstered by Rhode Island’s iGaming market launch in March 2024. In terms of legal sports betting, Americans wagered a first-quarter record of USD 36.86 billion on sports in Q1, generating USD 3.33 billion in quarterly revenue (more than 22% year-over-year). The growth compared to Q1 2023 was in part driven by new market launches in Kentucky, Maine, North Carolina, and Vermont.

Situation of state lotteries

About state lotteries, Vixio explains that these lotteries operate sports betting either directly or via a contracted operator or multiple partners in eight states (Connecticut, Delaware, Montana, New Hampshire, Ohio, Oregon, Rhode Island, Vermont) plus the District of Columbia. Mobile sports wagering is offered by lotteries or partners operating on their behalf in seven of the nine jurisdictions, with lottery-run sports betting limited to kiosks and other on-site wagers in Montana and Ohio. Lottery commissions also regulate sports betting in various states, including North Carolina and Virginia.

Six years after the Supreme Court’s ruling to overturn PASPA, state lotteries have generally failed to capture a meaningful portion of the sports betting market. Two state lotteries (DC and Oregon) have backed away from initial plans to operate their own sportsbooks by pulling the plug and instead partnering with FanDuel and DraftKings, respectively. The launch of FanDuel in DC last month leaves Sportsbook Rhode Island as the only native lottery sports-betting brand still active in the U.S. Meanwhile, several other lottery sports-betting initiatives have failed to get off the ground, including for kiosk or parlay products in Illinois, New Hampshire, and Louisiana.

With the District of Columbia and Oregon both reporting far greater revenue from mobile sports betting since switching from a lottery-run to a third-party sportsbook, it is hard to envisage too many other state lotteries taking the plunge into the market via their own offerings in the near future. As such, will state lotteries start to play a different role in the market, potentially through marketing partnerships with major brands? Elsewhere, it is to be seen if lotteries will seek to introduce more sports lottery-style products, along the lines of the longstanding football parlay offering of the Delaware Lottery, complementing their traditional draw and instant game offerings.

State lotteries that have shifted gears on sports betting

The District of Columbia Lottery launched its ill-fated GambetDC mobile sportsbook in 2020, but withdrew the offering in April of this year after the lottery’s primary technology vendor Intralot inked a sub-contract with U.S. market leader FanDuel.

As for the Oregon Lottery, it has launched its Scoreboard online betting platform in 2019, but took advantage of the opportunity to switch to DraftKings less than three years later, after DraftKings acquired the lottery’s contracted platform provider, SBTech. Annual revenue was up almost 150 percent in 2023 compared to 2021.

In 2019, legislation authorized the New Hampshire Lottery to contract with private operators to offer mobile and retail sports betting on its behalf, with the lottery also permitted to deliver sports wagering parlays and prop bets via its own retailer network. Five years later, the lottery’s planned Sports 603 offering has yet to get off the ground.

In Louisiana, alongside authorizing sports betting via casino operators, a 2021 state law also allowed the Louisiana Lottery Corporation to offer sports wagering via kiosks and a mobile platform. BetMGM was reportedly selected to run the operation on the lottery’s behalf before later declining to move forward, with lottery officials since indicating that the plans are on hold.

The state’s 2019 sports wagering law authorized the Illinois lottery to select a system provider to operate a network of sports betting kiosks on a pilot basis. The program also seemed unlikely to move forward given a requirement for USD 20 million upfront from the kiosk operator and the fact that wagers would be limited to parlays.