In this article, we will consider the valuable contributions of two recent remarkable reports: Market Forecast Outlook: Europe, North America and Latin America, by VIXIO GamblingCompliance, a relevant provider of independent legal, regulatory and business intelligence to the global gambling industry, and Total U.S. Gambling Spend by Category – 2022 study, by renowned boutique research and consulting firm Eilers & Krejcik Gaming, LLC.

Regulated U.S. online sports betting and gaming gross revenue jumped by 61% to an estimated USD 12.4 billion in 2022, blazing past the symbolically significant USD 10 billion mark as the U.S. overtook the UK to become the largest regulated online gambling market in the world within four years of the repeal of the Professional and Amateur Sports Protection Act of 1992 (PASPA). Gross revenue across 23 active online sports betting states soared by 91% year-on-year to an estimated USD 6.9 billion and, in doing so, overtook the parallel U.S. iGaming sector where GGR is estimated to have risen by 34% to USD 5.5 billion across a smaller footprint of seven states.

This latest balance shift reflects the differing fortunes of the two verticals in the legislative arena, with 14 new states having launched online sports betting operations since the start of 2020 versus an equivalent three in the iGaming arena.

The online sector’s growth has been driven by an unprecedented deluge of successful gambling expansion bills in recent years and a step change in consumer habits following the onset of COVID-19 that has been sustained amid a strong rebound in land-based casino revenue. On the sports betting side, strong growth in existing states such as Illinois, Tennessee and Virginia during 2022 was supported by sizeable contributions from newer online markets, including Arizona, Louisiana and, most notably, New York. The launch of online sports betting in Maryland, Kansas and Ohio during the 2022 NFL season was followed by the debut in Massachusetts (March 10th 2023), with these four states expected to collectively drive well over USD 1 billion in incremental gross revenue during 2023.

However, market growth from 2024 onwards will necessarily become more organic in nature. In fact, a lack of new markets has already constrained growth on the iGaming side. Just two additional states (Indiana and Iowa) are expected to go live over the next years.

CANADA’S LANDSCAPE: THE ONTARIO CASE

Over the border in Canada, Ontario became arguably the global online gambling industry’s most important new market upon its launch in April 2022, completing its transition from an OLG monopoly to a competitive model. That status is chiefly a result of Ontario’s sizeable population, exceeded by just four U.S. states, and a unique but ultimately “European-style” open licensing framework for a full product suite, with 73 licenses issued as of early February 2023.

The steady transition of major operators from Ontario’s grey market to the licensed sector resulted in quarterly online net revenue progressively improving from C$162 million (USD 121 million) in the second quarter of 2022, debut figures that were widely viewed as somewhat underwhelming, to C$267 million (USD 200 million) in Q3 and C$457 million (USD 342 million) in Q4.

GAMBLING SPENDING LED BY CASINOS

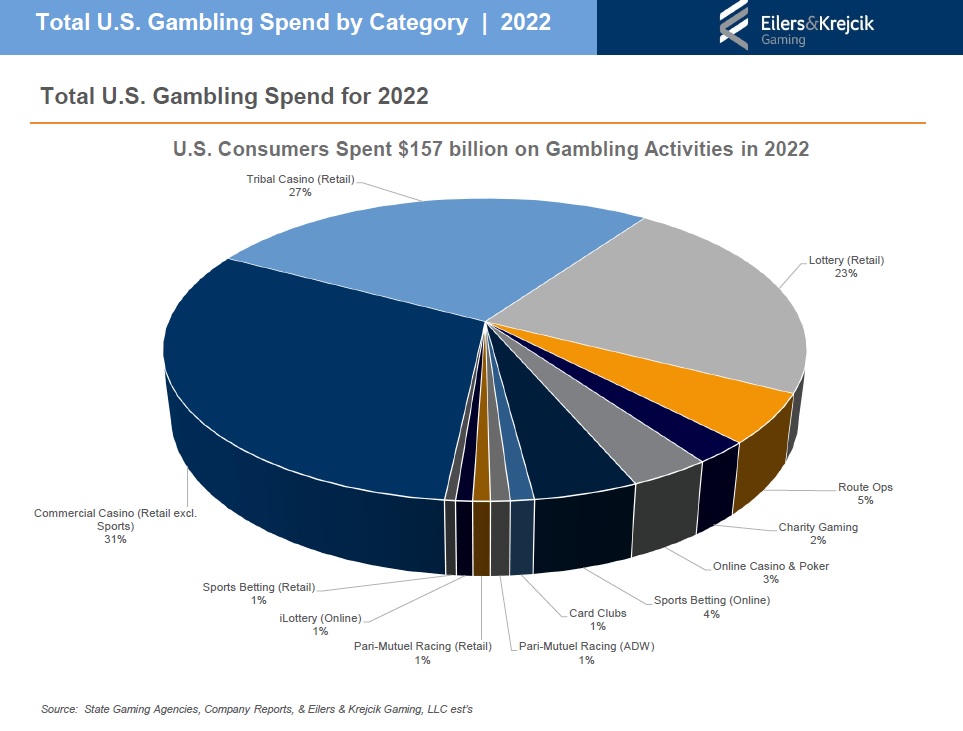

When focusing on people’s spending in gambling, it’s very interesting to take a look at the Total U.S. Gambling Spend by Category – 2022 report from Eilers & Krejcik Gaming. The company elaborated this annual report to provide a top-level view of the U.S. gambling market in terms of B2C revenue generated by market category, understanding revenue as total wagers less payouts (Gross Gaming Revenue, GGR).

This document shows that U.S. consumers spent USD 157 billion on gambling activities in 2022. Casinos captured 63% of the total GGR, followed by Lottery at 23%, then Distributed Gaming/Route Ops (5%), Sports Betting (5%), Charity (2%), and Racing (2%), with retail and online gambling spend combined for each category. The online channel (including online casino, poker, sports betting, iLottery, and pari-mutuel ADW) represented 9% of the total vs. 7% the prior year.

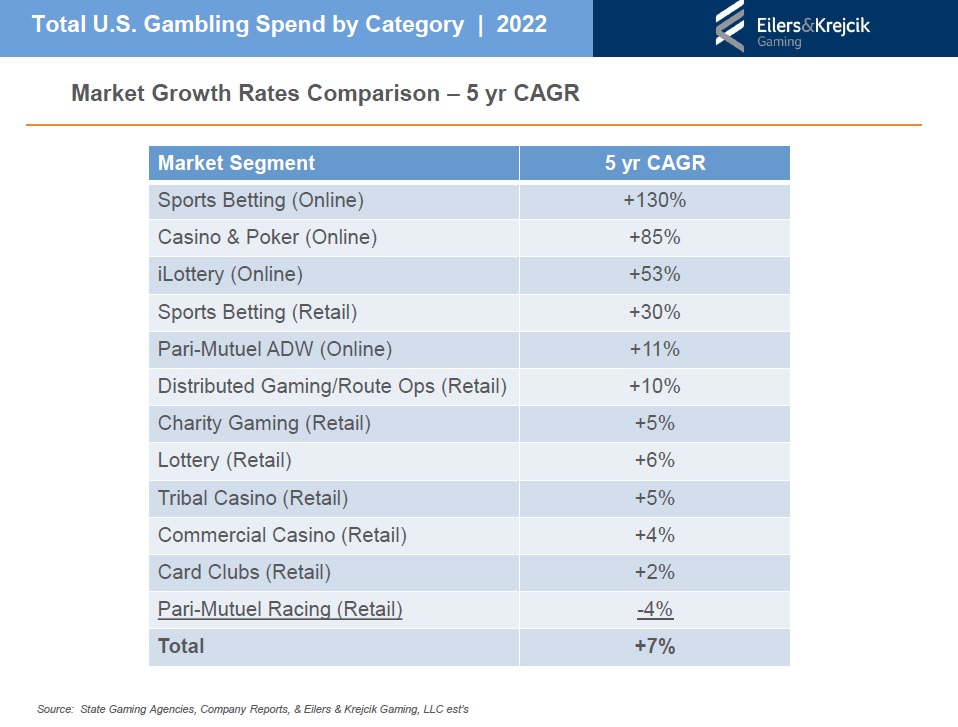

When considering Market Growth Rates Comparison for the last 5 years in terms of Compound Annual Growth Rate (CAGR), we can see different numbers by segment. Sports Betting (Online) had a CAGR of an astounding +130% over the last five years, followed by Casino & Poker (Online), with +85%; iLottery (Online), with +53%; Sports Betting (Retail), with +30%, and Pari-Mutuel ADW (Online), with +11%.

A FUTURE SCENARIO OF MORE EXPANSION

According to VIXIO GamblingCompliance estimates, regulated U.S. online gambling revenue will reach USD 23.8 billion in 2026, with online sports betting climbing at a compound annual rate of 21% to USD 14.8 billion, and iGaming expanding at an equivalent CAGR of 13% to USD 9 billion.

Excluded from this base case are potential online sports betting launches in California, Florida and Texas, as well as the plausible addition of iGaming in New York, with these potential new markets collectively representing multi-billion-dollar upside to the forecasts.

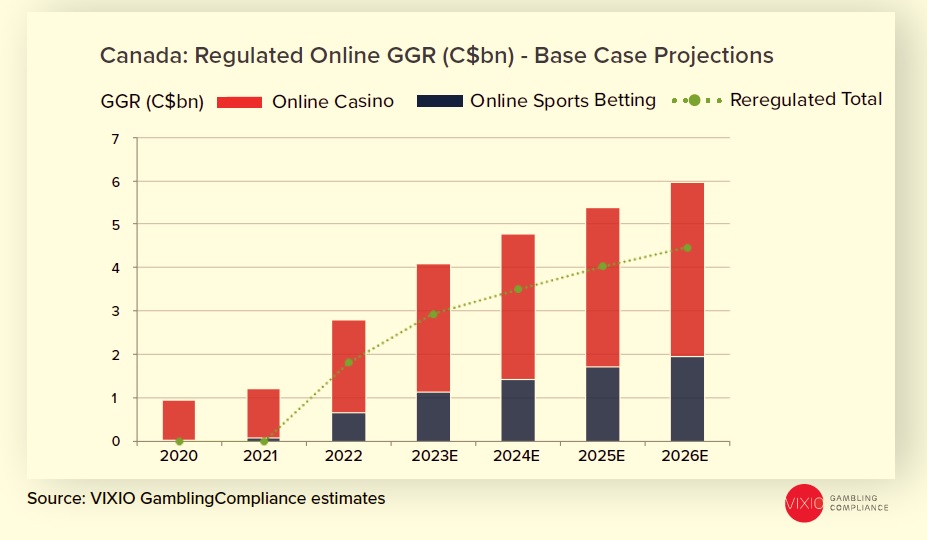

Regarding Canada, overall regulated online gambling revenue will reach just under C$6 billion (USD 4.5 billion) by 2026. A majority C$4.5 billion (USD 3.3 billion) of this total is expected to be generated in “re-regulated” competitive markets, with Ontario’s C$3 billion fully regulated system predicted to be followed by the introduction of competitive sports betting markets in Alberta, British Columbia and Manitoba over the next two to three years.

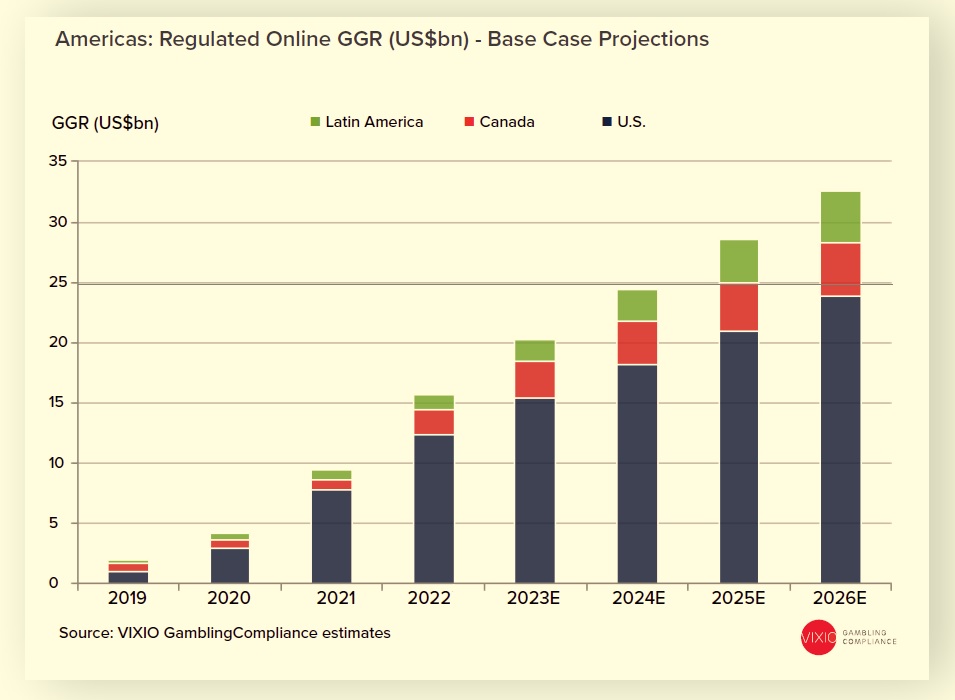

Taken together and focusing at a global level, VIXIO GamblingCompliance’s suite of interactive Forecasting Dashboards model anticipates 12% compound annual growth in regulated online gambling revenue across Europe, North America and Latin America from USD 45.5 billion in 2022 to USD 71.7 billion in 2026.

The addressable regulated online market opportunity in Europe and the Americas is therefore projected to grow by more than 250% or over USD 50 billion in absolute terms versus its pre-pandemic level of USD 20.4 billion in 2019.

In sum, ongoing legislative expansion and organic growth in the United States, complemented by sizable new market launches in Ontario and Brazil, is forecasted to more than double the broader Americas regulated “Total Addressable Market (TAM)” from USD 15.6 billion in 2022 to USD 32.5 billion by 2026.